Italy is a nation of homeowners that built one of Europe's oldest cooperative-housing movements — then let it shrink below one per cent of the stock. As renting reaches the salaried young, can the form be revived?

Read the profile

Where renting was never part of the plan

Italy built its post-war settlement around ownership. The family home, bought once and passed down, became the country's main store of wealth and a quiet substitute for a thin welfare state — a habit so deep that renting still reads, culturally, as a phase rather than a destination. That instinct shapes everything that follows: when housing costs climb here, the argument is less about rent regulation than about who can still buy, and what happens to the minority who cannot.

The tenure numbers carry that instinct in figures. About 70.8% of Italians are owner-occupiers and 29.2% are tenants — one of the higher ownership shares in Western Europe. Inside the rental base, public and non-profit housing accounts for just 4% of dwellings, and the cooperative slice for 0.8%: roughly 250,000 apartments held by about 450 active cooperatives. That leaves 24.4% of the stock in private rental. The non-market tier — cooperative plus public — comes to just 4.8% of all dwellings, among the slimmest in the region and the structural reason the affordability squeeze lands so hard on those shut out of ownership.

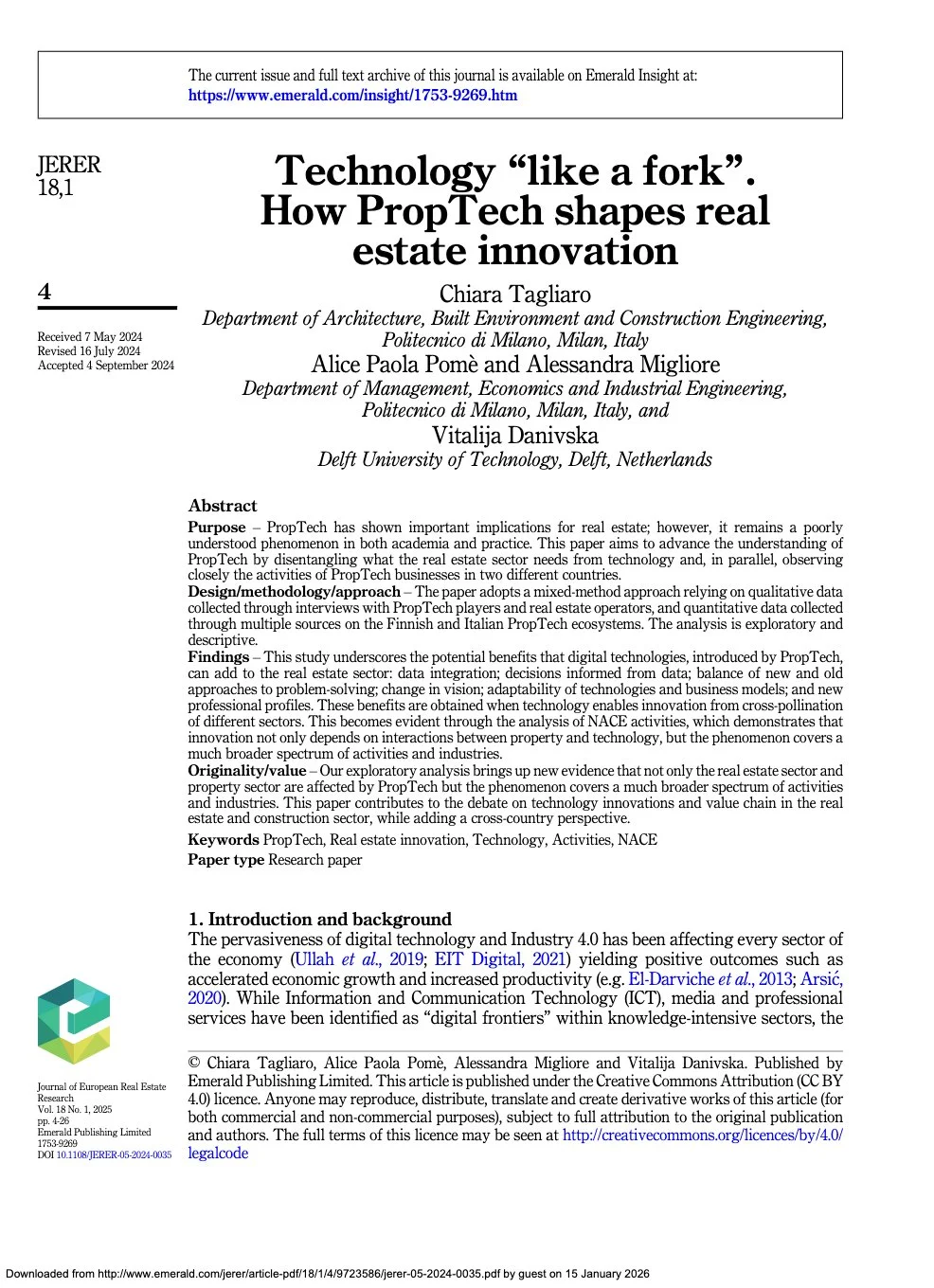

Italy's national tenure mix

Owners

Owner-occupier70.8%

Renters

Public & non-profit rental4.0%

Cooperative0.80%

Private rental24.4%

Roughly 4.2% of the national stock additionally carries an edilizia residenziale pubblica (public social-housing) or edilizia residenziale sociale (regulated affordable-housing) obligation — a public-affordability layer that overlaps the rental tiers shown above rather than forming a tenure of its own. Italy holds about 760,000 such public-housing units, the bulk run by regional Federcasa-affiliated agencies.

Share of national dwellings by tenure, resolved live from the geographic catalogue. Italy is a homeowner republic: more than seven in ten households own, the non-market rental tier is among the thinnest in Western Europe, and the cooperative slice — though historically deep — sits below one per cent of the national stock.

What social housing exists sits on top of that pie rather than beside it. Italy's edilizia residenziale pubblica (public residential housing) is a regulated layer — roughly 760,000 units, mostly run by regional Federcasa-affiliated agencies, let at controlled rents to eligible households. Add the newer edilizia residenziale sociale (social affordable housing) and the obligation covers about 4.2% of national stock. Around 35% of households would qualify for a regulated unit on income grounds — far more than the binding stock can ever house, so the queue, not the rent, is the rationing mechanism.

The rent ladder shows why the small non-market floor matters so much. Public-housing rents run at about €2.80 per square metre a month, cooperative rents at €4.80, the all-stock median at €8.50, newly-signed private contracts at €13.20, and furnished or serviced lets at €17.80. A cooperative tenancy costs roughly a third of an average private rent and barely a third of a fresh contract — which is precisely why a slice under one per cent of the stock carries an argument far larger than its size.

The national rent ladder in Italy

Public housing (ERP)

Cooperative

All-stock median

New contracts

Furnished / serviced

Net monthly rent per m² by tier (national figures; furnished is gross asking). The cooperative and public-housing floor sits at roughly a third of an all-stock private rent and well under half a freshly-signed contract — the structural gap that gives the small non-market tier its outsized importance in the tight cities.

Empty space and tourist lets pull in opposite directions. Italy's residential vacancy runs high — about 22.2% of dwellings, some six million empty buildings — but most of that sits in depopulating southern villages and inland hill towns, not in the cities where people actually need homes. In those cities, short-stay platforms strip supply the other way: across just the eight Italian cities the catalogue tracks closely, at least 46,096 dwellings are estimated to be in effectively full-time short-let use, a floor on a national figure that runs well higher in Rome, Florence and Venice. Office vacancy adds a further 13.5%, a pool of empty floor that conversion advocates eye in the tight northern markets.

“

The housing crisis is now permanently at the centre of the European debate.

Demand keeps the northern cities tight even as the country as a whole shrinks. Italy takes in around 492,000 inbound migrants a year against roughly 60,000 residential building permits — a supply gap widening across a stock of 31.2 million dwellings, concentrated in the metropolitan areas migration and internal mobility flow toward.

The burden has climbed past the poorest into the salaried young. Italy now records roughly 96,000 people in homelessness and about 35,000 court-ordered residential evictions a year, with arrears the dominant cause. But the sharper change is who feels exposed: a generation of renters in Milan, Bologna and Rome on permanent contracts who still cannot assemble a deposit or clear a mortgage stress-test, priced out of both buying and a tight private-rental market. The European housing-completions data underline how structural the squeeze is — Italy ranks last in Europe for new dwellings completed relative to need, a shortfall the journalistic record traces to a decade of near-frozen construction. The state's own diagnosis matches: the 2025 Piano Casa is framed explicitly around the "grey zone" of households who earn too much for public housing yet too little for the open market, an admission that the squeeze has moved into the middle.

From the tobacco workers of Bologna to undivided ownership

The Italian housing cooperative was born of mutual self-help, not the state. When tobacco-factory workers in Bologna founded one of the first cooperative di abitazione (housing cooperatives) in 1884, they were pooling wages to build what the market would not give them. Emilia-Romagna remains the movement's heartland. The Housing Europe survey of European cooperative housing places the Italian sector among the continent's oldest continuous traditions — roughly 400,000 dwellings delivered across more than a century, even if the form never reached the national scale it did in Austria or Scandinavia.

Two legal forms sit inside that tradition, and the distinction is the whole story. Most Italian cooperatives operate proprietà divisa (divided ownership): the cooperative builds at below-market cost using subsidy and tax exemptions, then transfers each flat to its member-owner, with resale restrictions that can run up to twenty years. The rarer and more durable form is proprietà indivisa (undivided ownership): the cooperative keeps the building permanently and leases to members indefinitely at cost, so the home can never be sold out from under the collective. It is this undivided slice — only around 40,000 rental dwellings — that behaves like permanent non-market housing, and it is the part the affordability debate keeps returning to.

Today the sector is leaner than its 1970s peak but still building. Across the federations it counts roughly 450 active housing cooperatives, about 250,000 cooperative apartments and a 624-million-euro mutual social-lending fund that recycles member savings into new development. Around 0.8% of Italians live in a cooperative home. The contraction has a clear cause: the 2007 financial crisis, market liberalisation and the devolution of housing policy to the Regioni (regions) cut state subsidy sharply, and the sector responded by managing and regenerating what it already held rather than chasing greenfield volume.

The movement organises under one umbrella, the Alleanza delle Cooperative Italiane (the Italian cooperative alliance), but through three historic federations. Legacoop Abitanti, founded in 1961 as ANCAB and the largest by membership, federates the cooperatives descended from the secular mutualist line. Federabitazione, inside Confcooperative Habitat, carries the Catholic-rooted tradition that split off in 1919. AGCI Abitazione holds the third, smaller strand. Between them the federations represent several thousand societies and well over half a million members — a wide base, even if most of their delivered units long ago became individually owned flats rather than collective rentals.

Where the form still innovates is in what Legacoop Abitanti calls the shift from a housing-centred to an inhabitants-centred model. Since the 1990s the federation has argued that meeting a housing need cannot be separated from urban quality, sustainability and social integration — so cooperative buildings are increasingly conceived as neighbourhood hubs for local welfare and culture, not just blocks of flats. The sector has also moved hard into comunità energetiche (renewable-energy communities), turning cooperative roofs and shared services into collectively-owned generation. The honest qualifier is scale: at 0.8% of the stock, the Italian cooperative is a demonstrator and a federated lobby more than a mass tenure, which is exactly why its next decade hinges on whether the state hands it land and patient capital again.

The €10bn Piano Casa, the grey zone, and who pays for the homes

Italian housing policy spent two decades drifting away from the centre, and the 2025 Piano Casa is the state pulling it back. After the 2007 crisis devolved most housing responsibility to the Regioni (regions) and left the public-housing budget to wither, the Meloni government has staked a national answer on a 10-billion-euro plan built on three pillars: recovering public housing, building regulated affordable homes, and crowding in private investment, with a headline target of more than 100,000 homes over ten years. Its first concrete promise is to recover 60,000 vacant council flats — units empty because they are sub-standard, illegally occupied or awaiting refit — within a year. Two decree-laws were tabled to carry it, one on the plan proper and one on evictions.

The plan's defining word is the "grey zone" — the households who earn too much to qualify for edilizia residenziale pubblica (public housing) yet too little to buy or rent on the open market. That framing concedes how far the squeeze has spread. The financing instruments aim squarely at it: a refinanced first-home guarantee fund offering a state backstop of up to 90% of a mortgage for large families, a 50% cut in notary fees on home transactions, and regulated-price construction for young families. In the first half of 2025 alone the guarantee fund underwrote over 38,000 mortgages worth 4.8 billion euros, up a fifth in number on the year before.

For cooperatives, the live question is whether the plan routes anything to them or simply subsidises ownership. The state's chosen vehicle for the non-market tier runs through Cassa Depositi e Prestiti (the national development bank) and its Fondo Investimenti per l'Abitare (FIA — the integrated housing-investment fund), which seeds the social-housing operators that have largely replaced direct cooperative building. Legacoop Abitanti has answered with its own pitch: a 1.4-billion-euro public-private platform — €850m of cooperative funds against €550m of public money — toward a 50,000-home social-housing programme, with the sector aiming to deliver a tenth of it. The proposal leans explicitly on European money, from Affordable Housing Initiative calls to European Investment Bank finance.

Two camps read the same crisis differently. The government's bet is on ownership and supply: guarantee young buyers' mortgages, unlock private capital, recover dormant stock, and let the market do the rest — a Piano Casa weighted toward helping people buy. The cooperative and social-housing camp, led by Legacoop Abitanti, argues that a country with a 4.8% non-market tier cannot guarantee its way out of a structural shortage, and presses instead for a permanent affordable-rental tier funded by a national platform and EU money. Both accept the grey zone exists; they disagree on whether the answer is a bigger mortgage or a bigger stock of homes nobody owns to sell.

Climate and reuse increasingly set the technical terms. The cooperative sector has positioned itself as a protagonist of the ecological transition — running comunità energetiche (renewable-energy communities) across its buildings, and pressing the case for circular-economy retrofit over demolition in a country whose housing stock averages fifty years old. The same logic points at Italy's empty offices and dormant council blocks as conversion candidates. How the PropTech and innovation layer reshapes that regeneration is itself contested, a debate the technology record frames as a tool that cuts both ways rather than a fix.

Milan timber, Bologna cohousing, a Roman barracks reborn

The clearest case for the Italian model is not the statute but a handful of buildings, clustered where the social-housing operators and the remaining cooperatives have land and partners — above all Milan, then Bologna, Turin and Rome. They show what the form can still do when patient capital and public ground line up behind it.

Milan is the showcase. Cenni di cambiamento was one of Europe's first social-housing schemes built in load-bearing timber — four CLT towers of regulated-rent and cohousing flats around a shared piazza, winner of the 2017 European Collaborative Housing Award and seeded by the Fondazione Housing Sociale model. A short walk into the city's regeneration pipeline, L'Innesto rises on the former Scalo Greco-Breda freight yard as Italy's first carbon-neutral housing sociale (social housing) project: some 400 affordable apartments plus student rooms, hybrid-timber and designed for disassembly, with shared kitchens and labs run by residents and local operators.

Bologna, fittingly, keeps the cohousing strand alive in the movement's birthplace. Porto 15 turned a disused civic building near the city centre into Italy's first public cohousing project — eighteen households sharing a courtyard, kitchen and workshops on a regulated lease. In Turin, the regeneration scene runs through the Future Urban Legacy Lab and operators like Homes4All, which buys and re-lets scattered flats to households in housing stress.

Rome shows the conversion case made physical. Porto Fluviale Rec House regularises a long-occupied former military barracks beside the Tiber into permanent public housing for the families who had squatted it — the reuse argument turned into homes rather than a slogan. Milan's DAR=CASA Società Cooperativa runs the everyday version of the same idea, managing public temporary housing in public-private partnership with the city: its Carbonia 3 court lets 48 affordable flats to families in emergency, young workers and students, with a resident social team woven in. Other regulated-rent schemes — Housing sociale Ex-Boero in Genoa, the ARIA development — fill out the picture across the north.

Behind the buildings sits a thin but distinct delivery machinery. Cassa Depositi e Prestiti and its housing fund supply patient capital; REDO SGR and the Fondazione Housing Sociale (FHS) structure and manage the schemes; Banca Etica and Coopfond lend on cooperative terms; Fondazione Cariplo underwrites the Milan pipeline; the Cooperativa Unitaria Abitare Milano and DAR=CASA hold the cooperative-management end; and the unibz Competence Centre for the Management of Cooperatives carries the research. It is a younger, foundation-and-fund-led ecosystem rather than a century-old federation of builders — which leaves the open question of whether Italy's next wave of permanent affordable homes comes from reviving the cooperative form or from the social-housing operators that now stand in its place.